Most people think life insurance is only useful after they die as a safety net for their loved ones. But what many don’t realize is this:

Modern life insurance can provide money while you’re still alive.

These features are called living benefits, and they can be life-changing when unexpected health issues or financial emergencies arise.

Let’s break it all down.

What Are Living Benefits?

These benefits are available on many modern policies, including:

• Term Life Insurance

• Whole Life Insurance

• Indexed Universal Life (IUL)

• Universal Life Insurance

• Final Expense Insurance

Living benefits help policyholders handle real-life challenges such as critical illness, disability, chronic conditions, or even retirement income needs.

How Can You Use Life Insurance While You’re Alive?

There are three primary ways to use life insurance while living:

1. Accelerated Death Benefits (ADB)

Access a portion of your death benefit early if you’re diagnosed with:

- A terminal illness

- Certain critical illnesses (heart attack, stroke, cancer)

- Chronic illnesses (unable to perform 2 of 6 Activity of Daily Living)

- Serious medical conditions that drastically reduce life expectancy

How it works:

The insurance company pays you part of your death benefit which is often up to 80% depending on the condition. Your beneficiaries receive the remaining balance when you pass.

Example:

If you have a $500,000 policy and suffer a major stroke, you may access $250,000–$400,000 now to pay for care, debts, or lost income.

2. Cash Value Access (for Permanent Policies)

Permanent life insurance like Whole Life or IUL builds cash value over time. This money can be used while you are alive through:

- Withdrawals (tax-advantaged)

- Policy loans (tax-free if managed properly)

- Surrenders (cashing out the policy)

People use cash value for:

- Retirement income

- Emergencies

- College funding

- Down payments on homes

- Business investments

Example:

Your IUL policy grows $60,000 in cash value. You borrow $20,000 tax-free to pay off high-interest credit cards. Your policy stays active as long as you keep it funded.

3. Long-Term Care or Chronic Illness Riders

Some life policies include long-term care features that allow you to use your death benefit to pay for:

- In-home care

- Assisted living

- Nursing home care

- Memory care

This can save you from paying $4,000–$9,000 per month out of pocket.

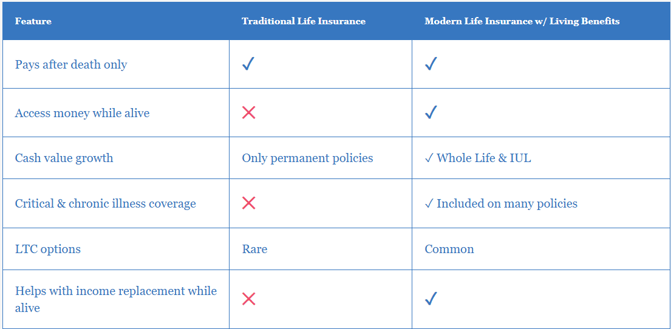

Living Benefits vs Traditional (Old-Style) Life Insurance

Living-benefit policies essentially give you life insurance + emergency protection + retirement flexibility in one package.

Who Benefits Most From Living Benefits?

Living benefits are particularly valuable for:

✔️ Families who depend on your income

If a heart attack, stroke, or cancer prevented you from working, living benefits give you access to cash exactly when you need it most.

✔️ People who want more than just a death benefit

Cash value allows for savings, loans, and retirement income planning.

✔️ Anyone without long-term care insurance

Long-term care riders can help cover extremely expensive elder-care costs.

✔️ Entrepreneurs and self-employed individuals

Cash value access can help stabilize a business, cover payroll, or provide funding.

✔️ People with a family history of major illnesses

Living benefits can provide financial relief during health battles.

Are Living Benefits Free?

Some are built into modern term and permanent policies at no cost.

Others may come as optional riders, such as:

- Chronic Illness Rider

- Critical Illness Rider

- Long-Term Care Rider

- Disability Waiver of Premium

In many cases, the cost is small compared to the protection they provide

Pros and Cons of Using Life Insurance While You’re Alive

Pros

- Access to cash during major health events

- Can replace lost income

- Protects family finances

- Cash value grows tax-deferred

- Loans can be tax-free

- Helps with retirement planning

Cons

- Advances reduce the final death benefit

- Policy loans must be managed carefully

- Not all term policies include cash value

Riders may increase premium slightly

Real-World Example: Why Living Benefits Matter

Scenario:

A 45-year-old Florida homeowner has a $400,000 life insurance policy with living benefits.

She suffers a heart attack and cannot work for 6 months.

With living benefits:

She takes $200,000 from her policy which is enough to cover medical bills, mortgage payments, and lost income.

Without living benefits:

Her family would have struggled financially while she recovers.

Living benefits act as a financial lifeline during life’s most challenging moments.

FAQs

1. Do all life insurance policies offer living benefits?

No. Many modern policies do, but older policies usually do not. Always check your contract.

2. Does using living benefits reduce the payout after death?

Yes, whatever amount you take early is deducted from the remaining death benefit.

3. Are living benefits taxable?

In many cases, no, but it depends on the type of benefit and how it’s accessed.

4. Can I add living benefits to an existing policy?

You may be able to, but it depends on the carrier. Some policies require a new application.

Final Thoughts: Life Insurance Isn’t Just for After Death. It’s Also For Living!

Life insurance with living benefits gives you something incredibly powerful:

-

Protection for your family after you die

-

Financial support for YOU while you're still alive

Whether you want to protect your family, build wealth, prepare for emergencies, or support your retirement, living-benefit life insurance can be a smart, flexible solution

.jpg?height=245&name=2149220326%20(1).jpg)